Commercial Vehicle Financing Market Overview

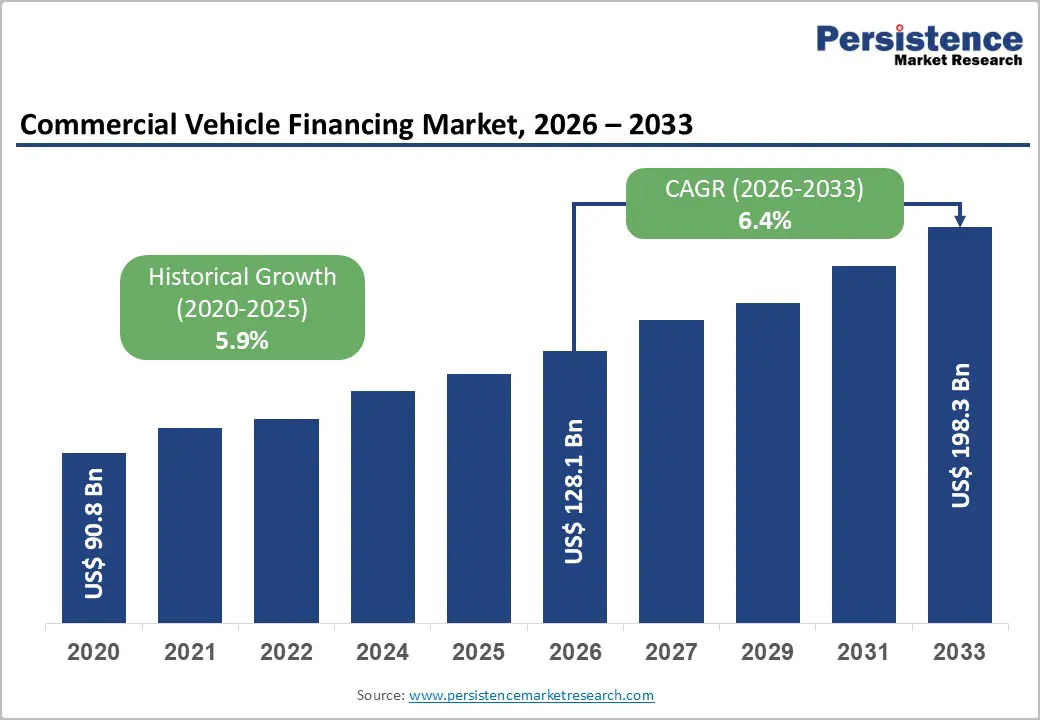

The global commercial vehicle financing market is experiencing steady expansion as logistics networks, e-commerce operations, fleet modernization programs, and vehicle electrification initiatives accelerate worldwide. The market size is projected to reach US$ 128.1 billion in 2026 and is expected to grow to US$ 198.3 billion by 2033, expanding at a CAGR of 6.4% between 2026 and 2033.

Commercial vehicle financing has become an essential financial solution for businesses operating trucks, vans, buses, and specialized vehicles by enabling fleet acquisition without significant upfront capital expenditure. Growing freight transportation demand, increasing replacement of aging commercial fleets, and rising adoption of electric commercial vehicles are reshaping financing models globally.

The expansion of digital lending platforms, artificial intelligence-based credit assessment, telematics-driven underwriting, and flexible leasing models is transforming the traditional commercial vehicle financing ecosystem. Financial institutions and captive finance companies are increasingly adopting technology-enabled solutions to improve loan approvals, reduce risk, and serve previously underserved owner-operator segments.

Asia Pacific remains the largest regional market, accounting for 38.7% share, supported by strong commercial vehicle production, infrastructure investments, and expanding non-banking financial company (NBFC) penetration. Meanwhile, North America and Europe are witnessing increased demand for EV-focused financing programs due to government emission regulations and fleet electrification targets.

Key Commercial Vehicle Financing Market Highlights

- Market Size (2026): US$ 128.1 billion

- Forecast Market Size (2033): US$ 198.3 billion

- Growth Rate: CAGR of 6.4% (2026–2033)

- Leading Provider Type: Banks with 47.2% market share

- Fastest-Growing Provider: NBFCs at 8.0% CAGR

- Dominant Financing Type: Loans/Hire Purchase with 64.5% share

- Fastest-Growing Financing Model: Operating Lease at 8.4% CAGR

- Leading Vehicle Segment: Light Commercial Vehicles (LCVs) with 45.6% share

- Fastest-Growing Vehicle Segment: Heavy Commercial Vehicles at 6.6% CAGR

- Largest Region: Asia Pacific with 38.7% share

Commercial Vehicle Financing Market Trends

Digital Lending Platforms Transforming Commercial Vehicle Financing

One of the most significant trends shaping the commercial vehicle financing market is the rapid adoption of digital lending platforms. Traditional commercial vehicle loans often required lengthy documentation processes, multiple verification steps, and extended approval timelines. However, fintech-based financing solutions are reducing loan processing periods from several weeks to only a few hours.

Digital lenders and NBFCs are integrating alternative data sources such as GPS tracking information, fuel purchase records, mobile payment history, vehicle utilization patterns, and tax records to evaluate borrower creditworthiness.

This technology-driven approach is particularly important in emerging markets where a significant proportion of commercial vehicle owners are small fleet operators or individual entrepreneurs without conventional financial documentation.

In countries such as India, Indonesia, and Vietnam, digital underwriting platforms are enabling lenders to expand credit access among millions of informal operators who were previously excluded from traditional banking systems.

Fleet Electrification Creating New Financing Opportunities

The transition toward electric commercial vehicles is creating a new growth avenue for financing providers. Governments worldwide are introducing stricter emission regulations and incentives to accelerate electric truck, bus, and van adoption.

In the United States, the Environmental Protection Agency’s heavy-duty vehicle emission regulations are encouraging fleet operators to replace diesel-powered trucks with electric alternatives. Since electric commercial vehicles typically have significantly higher purchase prices compared with conventional vehicles, financing requirements are increasing substantially.

The Inflation Reduction Act provides commercial clean vehicle incentives of up to US$ 40,000 per vehicle, improving the financial attractiveness of electric fleet investments.

European regulations requiring major reductions in heavy-duty vehicle emissions are also encouraging OEM finance companies such as:

- Volvo Financial Services

- Daimler Truck Financial Services

- PACCAR Financial

to introduce dedicated electric vehicle financing solutions.

These programs include flexible lease structures, battery warranties, and residual value guarantees designed to reduce financial risks associated with emerging EV technologies.

Market Dynamics Analysis

Growth Drivers

Expansion of E-Commerce and Logistics Infrastructure

The rapid growth of e-commerce is one of the strongest drivers of commercial vehicle financing demand. Increasing online shopping activity has created greater requirements for last-mile delivery fleets, warehouse transportation networks, and long-distance freight operations.

Global e-commerce sales surpassed US$ 5.8 trillion in 2023 and continue expanding, encouraging logistics companies to invest in fleet expansion. Rather than purchasing vehicles using internal funds, many businesses prefer financing solutions to maintain liquidity and optimize capital allocation.

The growth of digital commerce platforms, quick-commerce services, and same-day delivery models is particularly boosting demand for light commercial vehicles used in urban distribution.

Infrastructure development programs are further strengthening commercial vehicle procurement demand. India’s PM Gati Shakti initiative and China's logistics corridor investments are creating large-scale opportunities for vehicle financing providers.

Increasing Demand for Fleet Replacement and Modernization

Aging commercial vehicle fleets require regular replacement due to operational efficiency requirements, maintenance costs, and changing emission standards.

Companies are increasingly upgrading fleets with:

- Fuel-efficient vehicles

- Connected commercial vehicles

- Electric trucks and buses

- Advanced safety systems

Higher vehicle prices and advanced technology integration are increasing financing requirements, supporting market expansion through 2033.

Market Restraints

Basel IV Capital Requirements Affecting Bank Lending

Increasing regulatory capital requirements represent a challenge for traditional banking institutions involved in commercial vehicle financing.

Basel IV regulations are increasing capital requirements for certain lending categories, making commercial vehicle loans less attractive for some banks. Higher capital costs may reduce profitability and encourage financial institutions to reconsider their exposure to transportation asset financing.

As a result, market opportunities are shifting toward:

- NBFCs

- OEM captive finance companies

- Digital lenders

These providers often have greater flexibility in pricing, underwriting, and borrower segmentation.

Rising Credit Risk in Used Commercial Vehicle Financing

Used commercial vehicle financing is expanding rapidly, particularly in developing economies. However, this segment carries higher credit risks due to:

- Informal borrower profiles

- Limited financial documentation

- Irregular income patterns

- Vehicle depreciation concerns

In markets such as India, used vehicle financing portfolios are growing among NBFCs, increasing the importance of GPS-based monitoring and predictive credit analytics.

Financial institutions are increasingly using telematics and real-time vehicle data to improve repayment tracking and reduce loan defaults.

Market Opportunities

Fintech-Based Credit Scoring for Small Fleet Operators

A major opportunity exists among small commercial vehicle operators who lack access to traditional financing.

Across Asia Pacific, approximately 60–70% of commercial vehicle ownership is controlled by individual operators and small businesses. Many of these borrowers have limited access to formal banking services.

Fintech lenders are addressing this gap by using:

- Vehicle tracking data

- Digital payment history

- Fuel consumption records

- Tax filing information

- Business transaction data

These technologies enable more accurate risk assessment and expand financing access.

Companies such as Mahindra Finance and Shriram Finance are investing heavily in technology-enabled lending platforms to capture this underserved market.

Growth of Operating Lease and Fleet-as-a-Service Models

Operating leasing is emerging as the fastest-growing financing segment, expanding at an 8.4% CAGR through 2033.

The shift from vehicle ownership toward fleet-as-a-service models is being driven by:

- EV technology uncertainty

- Residual value concerns

- Corporate sustainability goals

- Lower upfront investment requirements

Operating leases allow companies to access modern fleets while avoiding ownership risks.

This model is especially attractive for logistics companies transitioning toward electric fleets.

Segment Analysis

Provider Type Analysis

Banks

Banks currently dominate the commercial vehicle financing market with a 47.2% share.

Their leadership is supported by:

- Strong lending capacity

- Established corporate relationships

- Dealer partnerships

- Competitive interest rates

Large fleet operators often prefer banks for high-value financing requirements.

However, regulatory pressure and changing borrower needs are gradually increasing competition from NBFCs and digital lenders.

NBFCs

NBFCs represent the fastest-growing provider category, expanding at 8.0% CAGR.

Their growth is supported by:

- Flexible repayment structures

- Faster approvals

- Strong rural and emerging market presence

- Alternative credit scoring models

NBFCs are particularly successful in financing small operators and used commercial vehicles.

Financing Type Analysis

Loans and Hire Purchase

Loans and hire purchase agreements dominate the financing segment with a 64.5% market share.

These financing structures remain popular because they provide:

- Vehicle ownership benefits

- Tax advantages

- Familiar repayment models

They continue to represent the preferred financing option for commercial operators globally.

Operating Lease

Operating leases are growing rapidly due to fleet modernization requirements and EV adoption.

Companies increasingly prefer leasing because it reduces:

- Balance sheet pressure

- Technology replacement risks

- Maintenance responsibilities

Vehicle Type Analysis

Light Commercial Vehicles (LCVs)

LCVs represent the largest vehicle category with a 45.6% share.

Growth is supported by increasing demand from:

- E-commerce delivery

- Food delivery services

- Urban logistics

- Small businesses

Their lower purchase price makes them accessible to individual operators and small enterprises.

Heavy Commercial Vehicles

Heavy commercial vehicles are expected to grow at a 6.6% CAGR.

Growth factors include:

- Highway freight expansion

- Infrastructure construction

- Electric truck financing programs

The higher value of heavy trucks creates significant financing opportunities.

Regional Market Insights

Asia Pacific Commercial Vehicle Financing Market

Asia Pacific dominates the global market with a 38.7% share.

Growth is supported by:

- Expanding logistics networks

- Increasing commercial vehicle production

- Infrastructure investments

- NBFC expansion

China Market

China represents one of the largest markets, valued at approximately US$ 21.8 billion in 2026.

Growth is supported by:

- Large commercial vehicle fleets

- Freight corridor development

- Manufacturing strength

India Market

India’s commercial vehicle financing market is estimated at US$ 12.9 billion in 2026.

The market is expanding due to:

- PM Gati Shakti infrastructure investments

- Digital lending growth

- NBFC penetration

- Electric bus financing programs

North America Market

North America is expected to grow at a 6.1% CAGR through 2033.

The United States remains the largest contributor, valued at approximately US$ 30.8 billion.

Key growth drivers include:

- Fleet electrification

- Logistics expansion

- Government EV incentives

- Heavy-duty truck replacement cycles

Europe Market

Europe accounts for approximately 19.4% share.

The region is driven by:

- Strict emission regulations

- ESG-focused lending

- Electric fleet transition

Germany remains a major market due to strong OEM presence from Daimler Truck, MAN, and Volkswagen Commercial Vehicles.

Competitive Landscape

The commercial vehicle financing market is moderately fragmented, with major players competing through digital transformation, EV financing solutions, and customized fleet programs.

Leading companies include:

- Volkswagen Financial Services AG

- Toyota Financial Services Corporation

- Daimler Truck Financial Services

- Wells Fargo Equipment Finance

- Volvo Financial Services

- PACCAR Financial Corp

- Shriram Finance Limited

- Mahindra Financial Services

- JPMorgan Chase & Co.

- BNP Paribas Leasing Solutions

- HSBC Holdings plc

- Mitsubishi UFJ Financial Group

- Deutsche Bank AG

- Tata Motors Finance

Companies are increasingly investing in:

- AI-powered underwriting

- Telematics-based risk management

- EV lease programs

- Digital customer platforms

Recent Strategic Developments

- Volvo Financial Services (September 2025): Introduced an electric truck lease program in Europe with flexible repayment structures to support fleet electrification.

- Shriram Finance (March 2024): Expanded commercial vehicle financing activities, particularly in used vehicle lending.

- PACCAR Financial (June 2024): Expanded EV truck financing programs across North America with battery warranty-linked risk solutions.

Conclusion

The global commercial vehicle financing market is entering a transformative growth phase driven by logistics expansion, fleet electrification, digital lending innovation, and emerging market credit expansion. The market is projected to grow from US$ 128.1 billion in 2026 to US$ 198.3 billion by 2033, supported by rising commercial transportation demand and evolving financing models.

While regulatory pressure and credit risks remain challenges, opportunities in fintech lending, operating leases, and electric vehicle financing are creating new growth pathways. Banks will continue leading the market, but NBFCs, captive finance providers, and digital lenders are expected to gain increasing influence through technology-driven solutions.

As businesses prioritize fleet efficiency, sustainability, and financial flexibility, commercial vehicle financing will remain a critical component of global transportation and logistics growth through 2033.