Flat Panel Displays Market Overview

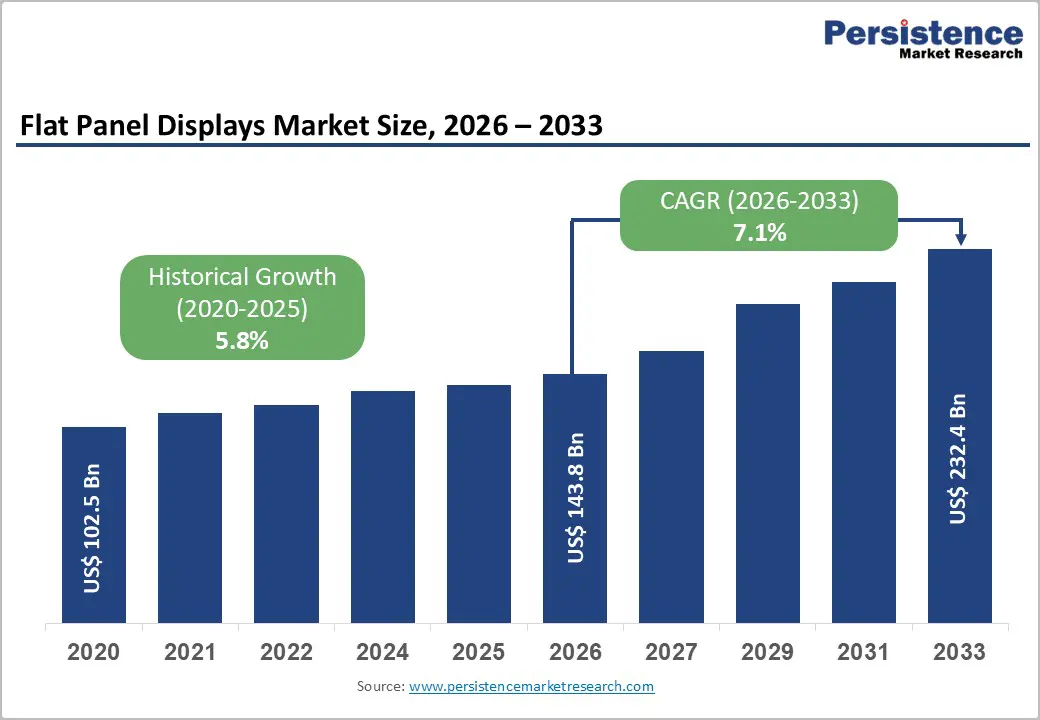

The global flat panel displays market size is expected to reach US$ 143.8 billion in 2026 and is projected to expand to US$ 232.4 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033. The market is witnessing strong expansion due to increasing demand for high-resolution, energy-efficient, and interactive display technologies across consumer electronics, automotive, healthcare, industrial automation, and digital signage applications.

Flat panel displays have become a fundamental component of modern digital ecosystems, powering smartphones, televisions, laptops, tablets, smart wearables, vehicle infotainment systems, medical equipment, and commercial displays. The rapid transition toward immersive digital experiences, rising adoption of OLED and QLED technologies, and increasing integration of advanced displays in electric vehicles are reshaping the competitive landscape.

The growing popularity of 4K and Ultra HD content, expansion of connected devices, and rising consumer preference for premium visual experiences are accelerating investments in next-generation display technologies. Additionally, manufacturers are focusing on flexible OLED, MicroLED, and quantum dot-based solutions to deliver improved brightness, contrast, durability, and energy efficiency.

Key Highlights of the Flat Panel Displays Market

- Market Size (2026): US$ 143.8 billion

- Forecast Value (2033): US$ 232.4 billion

- Growth Rate (2026–2033): CAGR of 7.1%

- Leading Region: Asia Pacific with approximately 43% market share in 2025

- Dominant Technology: LCD with nearly 42% market share in 2025

- Largest Application Segment: Smartphones & Tablets with approximately 34% market share in 2025

- Fastest-Growing Application: Automotive Displays

- Major Opportunity Areas: Healthcare displays, industrial automation, digital signage, and smart mobility solutions

Market Dynamics Driving Flat Panel Displays Growth

Rising Adoption of OLED and QLED Technologies Across Premium Consumer Electronics

The increasing adoption of advanced display technologies such as OLED (Organic Light Emitting Diode) and QLED (Quantum Dot Light Emitting Diode) is one of the primary factors driving the growth of the flat panel displays market.

OLED technology has gained significant momentum due to its superior picture quality, high contrast ratio, faster response time, thinner form factor, and ability to support flexible designs. Smartphone manufacturers are increasingly integrating OLED panels into premium and mid-range devices as consumers demand enhanced viewing experiences.

OLED surpassed LCD as the leading smartphone display technology in 2024, accounting for nearly 56% of smartphone display shipments. Leading companies such as Samsung Electronics Co., Ltd. and LG Display Co., Ltd. are investing heavily in OLED manufacturing capacity to address growing demand from smartphones, televisions, automotive displays, and IT devices.

LG Display’s investment of approximately US$ 925 million through 2027 to expand OLED production capabilities highlights the strategic importance of advanced display technologies in future market growth.

QLED displays are also gaining traction due to their improved brightness levels, color accuracy, and longer lifespan. These technologies are becoming increasingly popular in premium televisions, gaming monitors, and professional displays.

Automotive Digitalization Accelerating Display Demand

The transformation of traditional vehicle interiors into advanced digital cockpits is creating significant growth opportunities for flat panel display manufacturers.

Modern vehicles increasingly rely on multiple displays, including:

- Digital instrument clusters

- Infotainment screens

- Head-up displays

- Rear-seat entertainment systems

- Advanced Driver Assistance System (ADAS) interfaces

The global automotive display market is projected to grow from US$ 13.6 billion in 2025 to US$ 18.3 billion by 2030, driven by electric vehicle adoption and increasing demand for connected mobility solutions.

Electric vehicles are particularly accelerating display adoption as automakers integrate large-format touchscreens, curved displays, and intelligent cockpit systems. Premium automotive manufacturers are moving toward multi-display architectures that combine entertainment, navigation, vehicle controls, and safety information.

More than 32 million automotive displays were shipped in Q1 2024, reflecting strong demand for digital vehicle interfaces.

Flexible OLED and advanced LCD technologies are becoming increasingly important in automotive applications due to their durability, energy efficiency, and ability to support unique interior designs.

Growth of Smart Wearables Supporting Market Expansion

The rapid growth of smartwatches, fitness trackers, augmented reality devices, and foldable smartphones is further strengthening demand for advanced flat panel displays.

Flexible OLED technology has become a preferred solution for wearable devices due to its lightweight structure and ability to support curved and foldable designs.

Samsung shipped more than 12.9 million foldable smartphones in 2023, with approximately 80% featuring OLED panels, demonstrating strong consumer acceptance of flexible display technologies.

As wearable electronics continue to evolve, manufacturers are investing in ultra-thin, flexible, and energy-efficient display solutions to improve device performance and user experience.

Market Restraints Affecting Flat Panel Display Growth

High Manufacturing Costs of Advanced Display Technologies

Despite strong growth opportunities, high production costs associated with advanced display technologies remain a major challenge.

OLED and MicroLED manufacturing require sophisticated production equipment, advanced materials, and highly controlled manufacturing environments. OLED manufacturing equipment can cost 30–40% more than conventional LCD production systems, increasing capital expenditure requirements.

These high costs impact pricing and limit adoption among price-sensitive consumers and manufacturers, especially in developing markets across Latin America, Africa, and parts of South Asia.

Display companies must continuously improve manufacturing efficiency and reduce production costs to expand premium display technologies beyond flagship applications.

LCD Oversupply and Price Competition

The LCD market faces increasing pressure due to production oversupply and aggressive pricing competition, particularly from Chinese manufacturers.

Companies such as:

- BOE Technology Group

- China Star Optoelectronics Technology (CSOT)

- Tianma Microelectronics

have expanded production capacity significantly, leading to increased global supply and declining average selling prices.

China is expected to account for approximately 76% of global OLED production capacity by 2025, strengthening its influence over the global display supply chain.

Traditional display leaders in South Korea, Japan, and Taiwan are focusing on OLED, MicroLED, and specialized display applications to maintain profitability and market differentiation.

Emerging Opportunities in Flat Panel Displays Market

Expansion of Digital Signage and DOOH Advertising

The rapid adoption of digital signage across retail, transportation, corporate offices, and financial institutions is creating new growth opportunities.

Businesses are increasingly replacing traditional advertising methods with interactive digital displays to improve customer engagement.

Key application areas include:

- Retail advertising screens

- Banking information displays

- Smart kiosks

- Corporate communication boards

- Public transportation displays

The U.S. digital signage market continues to experience strong expansion, supported by increasing investments in interactive displays and customer experience technologies.

Demand for high-brightness, 4K, and OLED-based commercial displays is expected to increase as organizations prioritize digital transformation.

Healthcare and Industrial Applications Creating New Revenue Streams

Healthcare modernization is emerging as an important growth area for flat panel displays.

Medical facilities require high-performance displays for:

- Diagnostic imaging

- Surgical visualization

- Patient monitoring

- Medical information systems

Healthcare displays require exceptional color accuracy, brightness, resolution, and reliability, making premium LCD and OLED technologies highly suitable.

Industrial automation is also contributing to market growth. Manufacturing facilities increasingly rely on ruggedized displays for:

- Machine monitoring

- Industrial control systems

- Process automation

- Factory analytics

Industrial display adoption in the U.S. has recorded approximately 19% growth, reflecting rising demand for smart manufacturing solutions.

Technology Analysis

LCD Technology Maintains Market Leadership

LCD technology remains the dominant segment, accounting for approximately 42% of the flat panel displays market share in 2025.

The continued leadership of LCD is supported by:

- Cost-effective manufacturing

- Established supply chains

- Large-scale production capacity

- Wide application coverage

LCD remains widely used in:

- Televisions

- Computer monitors

- Automotive displays

- Commercial screens

Asia Pacific, particularly China, South Korea, and Taiwan, contributes more than 65% of global LCD production capacity.

However, OLED represents the fastest-growing technology segment due to increasing adoption in premium smartphones, automotive applications, and next-generation displays.

Application Analysis

Smartphones and Tablets Dominate Market Demand

The smartphones and tablets segment leads the flat panel displays market with approximately 34% market share in 2025.

More than 1.2 billion smartphones are shipped annually worldwide, creating continuous demand for display upgrades.

Manufacturers are increasingly adopting:

- AMOLED displays

- Flexible OLED panels

- High-refresh-rate screens

- Ultra-high-resolution displays

The Asia Pacific region remains the largest consumer market due to rising smartphone penetration and expanding middle-class populations.

Automotive Displays Represent the Fastest-Growing Segment

Automotive displays are expected to register the highest CAGR during 2026–2033.

Growth is driven by:

- Electric vehicle expansion

- Digital cockpit integration

- ADAS adoption

- Connected vehicle development

Automakers are increasingly partnering with display manufacturers to develop customized solutions for future mobility platforms.

Resolution Insights

Full HD Maintains Market Leadership

Full HD resolution holds approximately 38% market share in 2025 due to its balance between affordability, performance, and image quality.

It remains widely used across:

- Smartphones

- Laptops

- Mid-range televisions

- Commercial displays

However, the 4K/Ultra HD segment is growing rapidly due to increasing streaming content availability and declining panel prices.

Consumers are increasingly upgrading to ultra-high-definition displays for gaming and home entertainment applications.

Regional Market Insights

Asia Pacific Leads Global Market

Asia Pacific dominates the flat panel displays market with approximately 43% share in 2025.

The region benefits from:

- Strong manufacturing infrastructure

- Presence of major display producers

- Growing electronics consumption

China remains the largest production hub, while South Korea continues to lead OLED innovation.

India is emerging as a major growth market due to:

- Smartphone adoption

- Electronics manufacturing incentives

- Rising consumer spending

Vietnam is also becoming an important display manufacturing center, supported by investments from companies such as Samsung Display.

North America Market Outlook

North America is projected to experience the fastest CAGR during 2026–2033.

Growth factors include:

- Premium OLED adoption

- Automotive technology advancement

- Healthcare modernization

- Digital signage expansion

The U.S. accounts for approximately 85% of North America's flat panel display demand.

Competitive Landscape

The flat panel displays market is moderately consolidated, with major companies investing heavily in research and development to maintain technological leadership.

Leading companies include:

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- Sony Corporation

- Sharp Corporation

- Japan Display Inc.

- Universal Display Corporation

- AU Optronics Corporation

- Innolux Corporation

- Panasonic Corporation

- NEC Corporation

- E Ink Holdings Inc.

Companies are focusing on:

- OLED advancement

- MicroLED development

- Flexible display technology

- Supply chain optimization

- Strategic partnerships

Future Outlook of Flat Panel Displays Market

The global flat panel displays market is expected to experience sustained growth through 2033 as industries increasingly depend on advanced visualization technologies.

Future growth will be shaped by:

- Expansion of OLED and MicroLED technologies

- Increasing electric vehicle adoption

- Growth of smart retail and digital signage

- Healthcare digitization

- Industrial automation

- Development of flexible and wearable displays

As display technologies continue evolving, manufacturers that successfully combine innovation, cost efficiency, and application-specific solutions will gain a competitive advantage.

Conclusion

The global flat panel displays market is projected to grow from US$ 143.8 billion in 2026 to US$ 232.4 billion by 2033, expanding at a CAGR of 7.1%. Strong demand from consumer electronics, automotive digitalization, healthcare modernization, and commercial display applications is driving long-term market expansion.

While challenges such as high manufacturing costs and LCD pricing pressure remain, opportunities in OLED, automotive displays, digital signage, and industrial applications are creating new growth avenues.

With continuous innovation in flexible displays, ultra-high-resolution panels, and energy-efficient technologies, the flat panel displays industry is positioned to remain a critical component of the global digital transformation landscape.