Mobile Fronthaul and Backhaul Market Overview

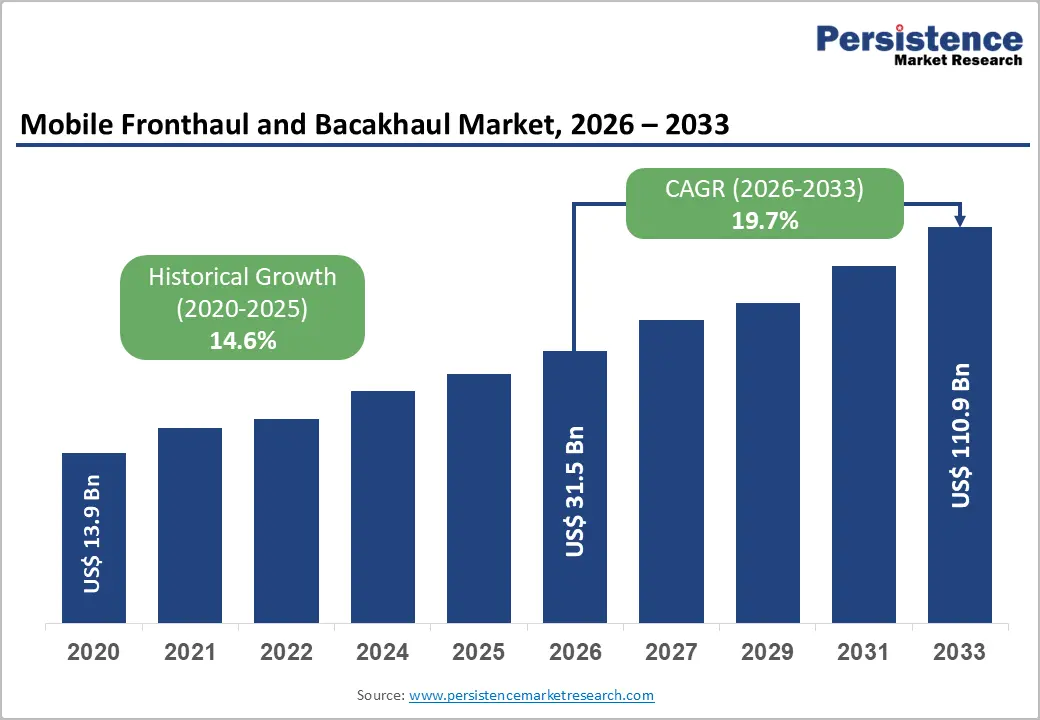

The global mobile fronthaul and backhaul market is witnessing rapid expansion as telecommunications operators worldwide accelerate 5G network deployments, upgrade transport infrastructure, and transition toward cloud-native and open network architectures. The market size is expected to reach US$31.5 billion in 2026 and is projected to expand to US$110.9 billion by 2033, registering a strong CAGR of 19.7% between 2026 and 2033.

The rapid evolution of mobile communication networks has created unprecedented demand for high-capacity, low-latency, and reliable transport solutions. Unlike previous generations of wireless networks, 5G requires significantly denser infrastructure, including small cells, edge computing nodes, and advanced radio architectures. These developments are increasing the importance of fronthaul and backhaul networks that connect radio access networks (RAN) with centralized and core network systems.

The growing adoption of Open RAN (O-RAN) architectures, rising mobile data consumption, expansion of private 5G networks, and increasing investments in fiber infrastructure are among the major factors accelerating market growth. Additionally, emerging technologies such as Cloud-RAN, artificial intelligence-driven network management, and LEO satellite backhaul are creating new opportunities for industry participants.

Key Highlights of the Mobile Fronthaul and Backhaul Market

- Market Size (2026): US$31.5 billion

- Forecast Market Size (2033): US$110.9 billion

- Growth Rate (2026–2033): 19.7% CAGR

- Leading Region: North America with approximately 38% market share

- Fastest Growing Region: Asia Pacific with a CAGR of 22.3%

- Dominant Technology: Fiber optic backhaul and optical fronthaul

- Largest Deployment Mode: On-premises infrastructure

- Fastest Growing Deployment: Cloud-based fronthaul solutions

- Major Opportunity: LEO satellite-based mobile backhaul expansion

Market Dynamics Driving Growth

Rapid Global 5G Deployment Increasing Demand for High-Capacity Transport Networks

The global rollout of 5G networks is the primary factor fueling demand for mobile fronthaul and backhaul infrastructure. Compared with 4G LTE networks, 5G requires significantly higher bandwidth, ultra-low latency, and improved reliability to support applications such as autonomous vehicles, industrial automation, smart cities, and immersive digital services.

5G networks rely heavily on dense small-cell deployments, particularly in urban environments. These small cells require efficient transport connectivity between radio units and centralized processing locations. In highly populated areas, cell sites may be positioned only 100–300 meters apart, creating a significant requirement for scalable fronthaul and backhaul solutions.

According to 3GPP specifications, 5G networks can deliver peak speeds of up to 20 Gbps, resulting in fronthaul requirements exceeding 25 Gbps per site in many deployments. Fiber-based solutions have become the preferred choice due to their superior bandwidth capacity, low latency, and scalability.

As operators continue expanding standalone 5G networks, investments in optical transport systems, high-speed routers, switches, and advanced network management platforms are expected to accelerate throughout the forecast period.

Open RAN Adoption Transforming Fronthaul Infrastructure

The emergence of Open Radio Access Network (O-RAN) technology is reshaping the mobile fronthaul ecosystem by replacing traditional proprietary RAN systems with open and interoperable components.

Traditional RAN architectures often depend on integrated solutions from single vendors. However, O-RAN separates network components into different functional units, including:

- Radio Units (RU)

- Distributed Units (DU)

- Centralized Units (CU)

This disaggregation increases flexibility but also creates greater demand for advanced fronthaul connectivity.

The O-RAN Alliance’s 7-2x functional split specification requires high-performance fronthaul networks capable of handling large volumes of data with strict latency requirements. As a result, operators are increasingly investing in optical fronthaul infrastructure.

Major companies such as Rakuten Mobile in Japan and Dish Network in the United States have deployed O-RAN-based networks, demonstrating commercial viability. With more than 300 organizations participating in the O-RAN Alliance ecosystem, adoption is expected to increase significantly through 2033.

Market Restraints

High Capital Investment Requirements for Fiber Deployment

Although fiber optic infrastructure offers unmatched performance, the cost associated with deployment remains a major challenge for operators.

Installing fiber networks requires substantial investment in:

- Fiber cables

- Civil construction

- Underground trenching

- Permits

- Network equipment

In dense urban areas, connecting every small cell with fiber infrastructure can cost more than US$50,000 per site, depending on construction complexity and regulatory requirements.

These high costs can slow network expansion, particularly in developing regions where operators face financial constraints.

While fiber remains essential for high-performance 5G networks, many operators continue using hybrid approaches combining fiber, microwave, and satellite technologies.

Spectrum and Interference Challenges Affecting Microwave Backhaul

Microwave backhaul remains an important connectivity solution because it offers faster deployment and lower installation costs compared with fiber. However, increasing network density is creating challenges related to spectrum availability and interference.

Dense urban 5G environments require multiple high-capacity links operating within limited spectrum resources. As more operators deploy microwave systems, interference management becomes increasingly complex.

Regulatory coordination requirements established by organizations such as the International Telecommunication Union (ITU) can also delay deployment timelines.

As a result, microwave solutions are expected to remain valuable for specific applications but may face limitations in ultra-high-capacity 5G environments.

Emerging Opportunities in the Mobile Fronthaul and Backhaul Market

LEO Satellite Backhaul Expanding Rural 5G Connectivity

One of the most promising opportunities in the market is the integration of Low Earth Orbit (LEO) satellite technology for mobile backhaul.

Fiber deployment is often economically challenging in rural and remote regions due to difficult terrain and low population density. LEO satellite networks provide an alternative solution by delivering high-speed connectivity with significantly lower latency compared with traditional satellite systems.

Companies such as:

- SpaceX Starlink

- Amazon Project Kuiper

are developing large satellite constellations capable of supporting broadband and mobile connectivity applications.

Starlink has deployed thousands of satellites globally, achieving latency levels below 40 milliseconds, making satellite backhaul suitable for many mobile network applications.

Government programs, including the U.S. USDA ReConnect Program and Europe’s IRIS² satellite initiative, are supporting satellite connectivity expansion and creating new opportunities for backhaul providers.

Cloud-RAN and Virtualized Fronthaul Creating Software Opportunities

The transition toward cloud-native network architectures is creating new revenue opportunities beyond traditional hardware infrastructure.

Cloud-RAN (C-RAN) allows operators to centralize network processing functions while using software-based management platforms. Combined with:

- Network Function Virtualization (NFV)

- Multi-access Edge Computing (MEC)

- Artificial intelligence-based automation

cloud-based fronthaul solutions enable operators to improve efficiency and reduce operational costs.

Companies such as Nokia, Mavenir, and Ericsson are developing cloud-native platforms that allow dynamic resource allocation and automated network optimization.

As operators move toward autonomous networks, software-defined transport management is expected to become a major growth area.

Segment Analysis

By Technology Type: Fiber Optic Solutions Dominate

Fiber optic backhaul and optical fronthaul represent the leading technology segment, accounting for approximately 40% of the combined market share.

Fiber technology dominates because it provides:

- Extremely high bandwidth

- Low latency

- Long-distance transmission capability

- High reliability

Modern optical transport technologies using DWDM can support capacities exceeding 100 Gbps, making fiber essential for future 5G and beyond networks.

Leading fiber infrastructure providers include:

- Ciena Corporation

- Corning Incorporated

- Infinera Corporation

By Component: Hardware Leads Market Demand

Hardware components account for approximately 55% of total market revenue.

Major hardware categories include:

- Optical transceivers

- Routers

- Switches

- Fiber cables

- Fronthaul gateways

- Microwave radio systems

The physical infrastructure required for 5G deployment ensures continued demand for hardware solutions.

Companies including Ericsson, Nokia, Cisco, and Juniper Networks provide advanced transport hardware platforms for global operators.

By Deployment Mode: On-Premises Infrastructure Dominates

On-premises deployment currently represents around 62% of the market.

Operators continue to rely on dedicated infrastructure because mobile transport networks require:

- High reliability

- Security

- Low latency

- Direct operational control

However, cloud-based deployment is growing rapidly due to increasing adoption of Cloud-RAN and virtualized network architectures.

By Application: Telecommunications Sector Leads

The telecommunications segment accounts for approximately 58% of market revenue.

Mobile operators are investing heavily in transport infrastructure to support:

- 5G networks

- Small-cell deployments

- Enterprise connectivity

- Network expansion

Private 5G networks for industries such as manufacturing, logistics, and energy are expected to become important growth contributors.

Regional Market Analysis

North America Mobile Fronthaul and Backhaul Market

North America is the leading regional market, accounting for approximately 38% share.

Growth is supported by:

- Large-scale 5G deployments

- Fiber infrastructure expansion

- O-RAN adoption

- Government broadband investments

The U.S. market is estimated at approximately US$9.2 billion in 2026, driven by C-band spectrum utilization and the US$42.45 billion BEAD broadband program.

Major telecom operators including Verizon, AT&T, and T-Mobile continue investing in advanced transport networks.

Asia Pacific Market Growth

Asia Pacific represents the fastest-growing region with a projected CAGR of 22.3%.

Growth factors include:

- China’s massive 5G infrastructure deployment

- India’s rapid network expansion

- Japan’s O-RAN leadership

China leads the regional market with approximately US$13 billion in 2026, supported by millions of installed 5G base stations.

India’s market is expected to reach around US$3.5 billion in 2026, driven by investments from Reliance Jio and Bharti Airtel.

Japan continues advancing cloud-native and open network technologies through companies such as Rakuten Mobile.

Competitive Landscape

The mobile fronthaul and backhaul market includes global telecom equipment leaders, optical networking companies, and emerging software providers.

Major players include:

- Huawei Technologies Co., Ltd.

- Ericsson

- Nokia Corporation

- Cisco Systems, Inc.

- ZTE Corporation

- Samsung Electronics

- NEC Corporation

- Juniper Networks

- Fujitsu Limited

- Ciena Corporation

- Infinera Corporation

- Corning Incorporated

- Mavenir Systems

- Ribbon Communications

- Ceragon Networks

- Siklu

Companies are focusing on:

- O-RAN-compatible solutions

- AI-powered network automation

- Cloud-native transport platforms

- High-capacity optical technologies

Recent Industry Developments

January 2025: Nokia launched its next-generation AirScale Fronthaul Gateway supporting 25G/100G optical fronthaul for O-RAN 7-2x deployments.

October 2024: Ciena expanded partnerships with Asia Pacific operators to deploy advanced optical transport platforms supporting 400G/800G network upgrades.

March 2024: Mavenir secured US$100 million investment to accelerate cloud-native O-RAN and RIC platform development.

Future Outlook of Mobile Fronthaul and Backhaul Market

The mobile fronthaul and backhaul market is entering a high-growth phase driven by global 5G expansion, increasing data consumption, and the transformation toward open, cloud-based network architectures.

While high deployment costs and infrastructure challenges remain, advancements in fiber technology, satellite connectivity, virtualization, and artificial intelligence are creating significant growth opportunities.

Between 2026 and 2033, telecom operators, infrastructure providers, and technology vendors will continue investing in next-generation transport networks to support the future of connected societies.

With the market projected to reach US$110.9 billion by 2033, mobile fronthaul and backhaul infrastructure will remain a critical foundation for global digital transformation.