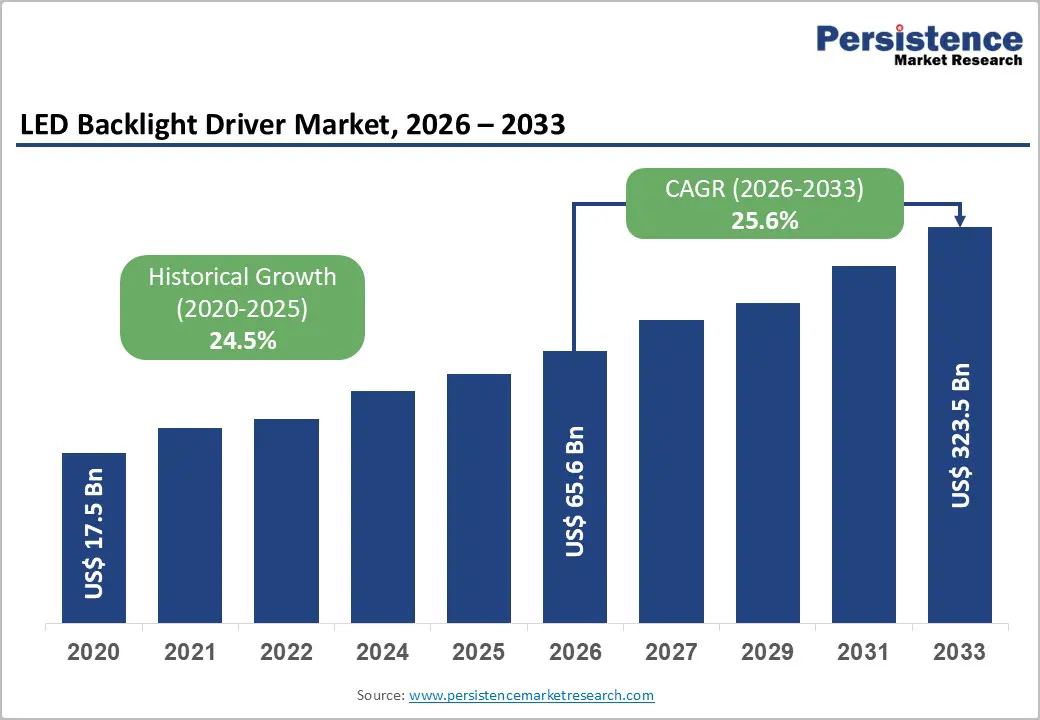

The global LED backlight driver market is entering a transformative phase as industries worldwide accelerate the adoption of energy-efficient lighting systems, smart infrastructure, and advanced display technologies. According to recent market analysis, the LED backlight driver market is expected to grow from US$65.5 billion in 2026 to US$323.5 billion by 2033, registering an impressive CAGR of 25.6% during the forecast period.

LED backlight drivers play a critical role in modern lighting and display systems by regulating current and voltage supplied to LEDs. Whether powering residential lighting, commercial buildings, automotive headlamps, televisions, smartphones, or industrial displays, these components ensure consistent brightness, enhanced efficiency, and longer operational life.

The growing replacement of conventional lighting technologies, rising investments in smart cities, expanding consumer electronics production, and increasing demand for automotive LED applications are creating substantial opportunities for manufacturers across the value chain.

Market Overview

The LED backlight driver market has become one of the fastest-growing segments within the semiconductor and lighting industries. As governments worldwide continue implementing strict energy efficiency regulations and sustainability initiatives, LED technology has become the preferred lighting solution.

Unlike traditional lighting systems, LEDs require sophisticated driver circuits capable of maintaining stable current regardless of voltage fluctuations. These drivers improve illumination quality while extending LED lifespan, making them indispensable across residential, commercial, automotive, healthcare, and industrial sectors.

The increasing adoption of Mini-LED and Micro-LED display technologies is further accelerating demand for advanced multi-channel LED driver integrated circuits (ICs), particularly in premium televisions, gaming monitors, automotive displays, and portable electronics.

Key Market Statistics

- Market Value (2026): US$65.5 Billion

- Forecast Value (2033): US$323.5 Billion

- CAGR (2026–2033): 25.6%

- Leading Region: Asia Pacific (45% market share)

- Dominant Supply Type: Constant Current LED Drivers (68%)

- Leading Application: General Lighting (48%)

- Fastest Growing Application: Automotive Lighting

These figures highlight the remarkable growth potential driven by innovation, regulatory support, and rising global LED penetration.

Why LED Backlight Drivers Are Becoming Essential

Every LED lighting system requires precise electrical regulation. LED backlight drivers convert incoming electrical power into controlled current that protects LEDs from damage while delivering stable illumination.

Their primary benefits include:

- Improved energy efficiency

- Longer LED lifespan

- Better thermal management

- Consistent brightness

- Enhanced color accuracy

- Reduced maintenance costs

As manufacturers develop smarter lighting products and advanced display technologies, LED drivers are evolving into intelligent control systems capable of communication, diagnostics, and remote management.

Major Growth Drivers

Global Shift Toward Energy-Efficient Lighting

Governments worldwide continue to phase out incandescent and halogen bulbs through stricter efficiency regulations.

Programs introduced by:

- European Union Ecodesign Directive

- U.S. Department of Energy (DOE)

- India's UJALA Scheme

- China's Energy Efficiency Programs

have significantly accelerated LED adoption across residential and commercial sectors.

According to the International Energy Agency (IEA), LEDs already account for more than half of global lighting sales, and this share is expected to exceed 80% before the decade ends.

Each new LED installation creates direct demand for LED driver technologies.

Rapid Expansion of Consumer Electronics

Modern consumer electronics increasingly rely on LED backlighting.

Applications include:

- Smartphones

- Tablets

- Smart TVs

- Gaming monitors

- Laptops

- Wearables

- Digital signage

Premium electronics manufacturers continue transitioning toward Mini-LED and Micro-LED displays, requiring highly sophisticated driver ICs capable of controlling hundreds or even thousands of LED zones.

This trend significantly increases semiconductor content per device.

Automotive Industry Driving Premium Growth

Automotive lighting represents the fastest-growing application within the market.

Today's vehicles increasingly incorporate:

- Adaptive Driving Beam (ADB) headlights

- Matrix LED lighting

- Ambient interior lighting

- Digital dashboards

- Infotainment displays

- Head-Up Displays (HUDs)

Modern matrix headlights may contain 32 to 84 individually addressable LED segments, each requiring dedicated multi-channel driver ICs.

As electric vehicles become mainstream, LED content per vehicle continues rising rapidly.

Smart Cities and Intelligent Buildings

Governments worldwide are investing heavily in smart infrastructure.

Smart lighting systems now integrate:

- Occupancy sensors

- Motion detection

- Daylight harvesting

- Remote monitoring

- Wireless control

- Energy analytics

Intelligent LED drivers supporting DALI-2, Zigbee, Bluetooth Mesh, and Thread communication protocols are becoming standard components within commercial buildings and municipal lighting projects.

Market Challenges

Thermal Management Complexity

As LEDs become more powerful and compact, driver ICs generate greater heat densities.

Manufacturers must simultaneously achieve:

- Higher efficiency

- Smaller form factors

- Lower electromagnetic interference

- Better heat dissipation

Balancing these requirements increases engineering complexity and production costs.

Semiconductor Supply Chain Risks

The semiconductor shortages experienced during 2020–2022 exposed vulnerabilities across the LED driver industry.

Driver ICs compete with numerous analog semiconductor products for mature manufacturing capacity.

Although supply conditions have improved, manufacturers remain focused on:

- Supply diversification

- Localized manufacturing

- Strategic inventory management

to minimize future disruptions.

Emerging Market Opportunities

Connected Lighting Systems

One of the biggest opportunities lies in intelligent LED drivers capable of network communication.

Advanced drivers now support:

- DALI-2

- Bluetooth Mesh

- Zigbee

- Thread

- Wireless dimming

- Cloud connectivity

The U.S. Department of Energy estimates connected lighting systems can reduce commercial building energy consumption by an additional 40–50% beyond standard LED savings.

These premium smart drivers command significantly higher profit margins.

Automotive Electronics

Automotive semiconductor content continues growing rapidly.

Future vehicles will require LED drivers for:

- Autonomous driving systems

- Matrix headlights

- Cabin lighting

- Digital displays

- Rear entertainment systems

- Exterior signature lighting

Automotive-qualified (AEC-Q100) driver ICs represent one of the industry's highest-value product categories.

Segment Analysis

By Supply Type

Constant Current LED Drivers Lead the Market

Constant current drivers account for approximately 68% of market share.

Their popularity stems from the fact that LEDs operate based on controlled current rather than voltage.

Benefits include:

- Stable illumination

- Longer lifespan

- Improved efficiency

- Better thermal stability

- Enhanced color consistency

Major manufacturers continue expanding constant-current product portfolios for industrial, residential, and automotive applications.

By Luminaire Type

Integral Modules Dominate

Integral LED modules contribute around 34% of total revenue.

These systems integrate:

- LED arrays

- Driver circuitry

- Thermal management

into a single optimized module.

Benefits include:

- Simplified installation

- Higher reliability

- Improved performance

- Compact product design

Commercial lighting manufacturers increasingly prefer integrated solutions.

By Application

General Lighting Maintains Leadership

General lighting represents approximately 48% of total market demand.

Applications include:

- Residential lighting

- Commercial buildings

- Street lighting

- Industrial facilities

- Educational institutions

- Healthcare infrastructure

Government LED replacement initiatives continue fueling widespread deployment.

Meanwhile, automotive lighting remains the fastest-growing segment due to premium vehicle technologies.

Regional Insights

Asia Pacific Leads Global Market

Asia Pacific accounts for approximately 45% of global market share, making it the industry's largest regional market.

Growth is supported by:

- China's manufacturing leadership

- India's national LED deployment programs

- Japan's advanced electronics sector

- Expanding Southeast Asian production

China remains both the world's largest producer and consumer of LED driver ICs.

India's UJALA and Street Lighting National Programme have collectively deployed hundreds of millions of LED products, generating enormous driver demand.

North America

North America continues investing heavily in:

- Commercial retrofits

- Smart buildings

- Automotive electronics

- Energy-efficient infrastructure

Strong DOE regulations and ENERGY STAR programs continue supporting market expansion.

The United States remains the region's largest contributor.

Europe

Europe's market growth is driven by:

- EU Ecodesign regulations

- Green Deal initiatives

- Building energy standards

- Automotive innovation

Germany leads regional demand due to its automotive manufacturing ecosystem and strong industrial lighting sector.

France and the United Kingdom also contribute significantly through smart city investments and commercial building modernization.

Middle East & Africa

The Middle East and Africa represent the fastest-growing regional market.

Key growth factors include:

- Smart city projects

- Vision 2030 initiatives

- Infrastructure modernization

- Urban development

- LED street lighting deployment

Countries such as Saudi Arabia and the UAE continue investing heavily in intelligent lighting systems.

Competitive Landscape

The LED backlight driver market remains moderately fragmented, with both global semiconductor companies and specialized LED driver manufacturers competing through innovation.

Leading companies include:

- Philips N.V. (Signify)

- Osram GmbH

- Texas Instruments

- ON Semiconductor (onsemi)

- Rohm Semiconductors

- STMicroelectronics

- Infineon Technologies AG

- Macroblock Inc.

- Maxim Integrated

- ERP Power LLC

- Cree Inc.

- General Electric

Competition increasingly focuses on:

- High conversion efficiency

- Automotive-grade certification

- Smart connectivity

- Mini-LED compatibility

- AI-enabled dimming

- Integrated wireless communication

Manufacturers continue investing heavily in research and development to maintain competitive advantages.

Recent Industry Developments

Recent product launches demonstrate the market's rapid pace of innovation.

In March 2025, Texas Instruments introduced the TPS92520-Q1, a dual-channel automotive LED matrix driver featuring integrated diagnostics and AEC-Q100 Grade 1 qualification for adaptive driving beam applications.

Earlier, in October 2024, ON Semiconductor launched the NCP5397B multi-string LED backlight driver, supporting premium Mini-LED television panels with precision current balancing and advanced fault detection capabilities.

These developments reflect growing demand for intelligent, high-performance LED driver solutions across automotive and display markets.

Future Outlook

The future of the LED backlight driver market appears exceptionally promising as global industries continue prioritizing energy efficiency, smart infrastructure, and digital transformation.

Emerging technologies such as Mini-LED displays, Micro-LED televisions, autonomous vehicles, connected lighting systems, and intelligent buildings will significantly increase demand for advanced driver ICs capable of delivering higher efficiency, better thermal performance, and seamless wireless connectivity.

At the same time, regulatory pressure to reduce carbon emissions and improve building energy efficiency will continue accelerating LED adoption worldwide.

Manufacturers that focus on innovation, automotive-grade solutions, IoT integration, and high-efficiency power management are expected to capture the greatest share of future market growth.

Conclusion

The global LED backlight driver market is poised for remarkable expansion, growing from US$65.5 billion in 2026 to US$323.5 billion by 2033 at a robust 25.6% CAGR. Rising demand for energy-efficient lighting, smart buildings, connected lighting systems, consumer electronics, and advanced automotive applications is reshaping the industry. As LED technology continues to replace conventional lighting and intelligent driver solutions become more sophisticated, the market will remain a cornerstone of innovation in the semiconductor and electronics ecosystem. Organizations that invest in high-performance, connected, and automotive-grade LED driver technologies are well-positioned to benefit from this long-term growth trajectory.