The global data center rack market is entering a period of sustained expansion as organizations continue investing in cloud computing, artificial intelligence (AI), edge computing, and digital infrastructure. Data center racks form the backbone of modern IT facilities, providing secure, organized, and efficient housing for servers, networking equipment, storage systems, and power distribution units.

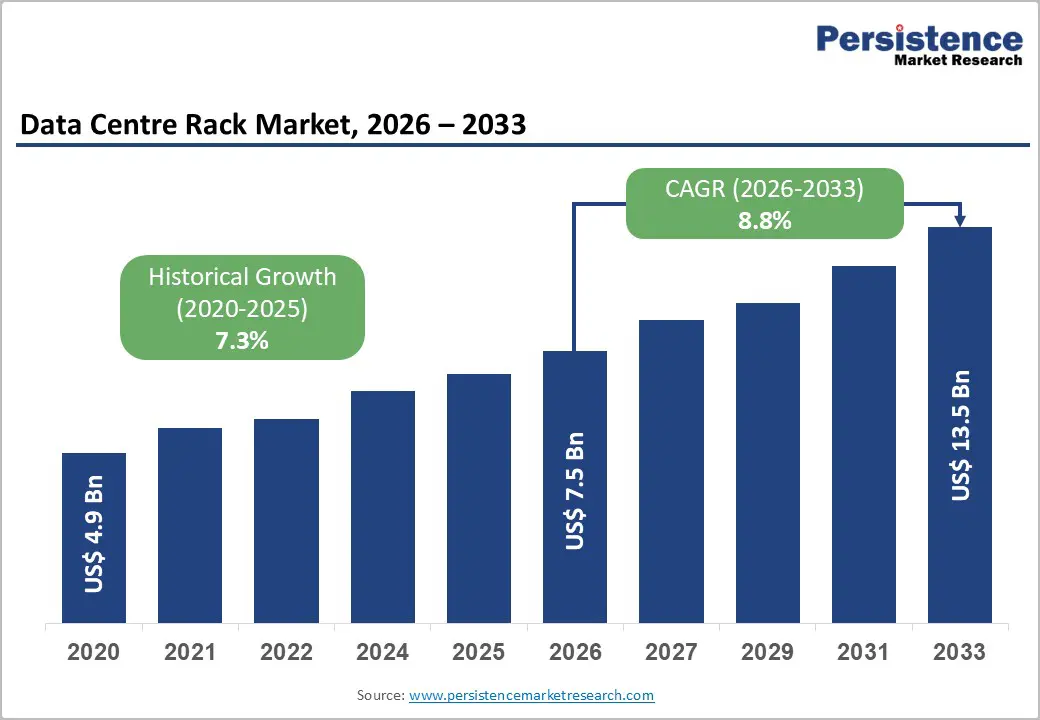

According to market estimates, the global data center rack market is expected to reach US$ 7.5 billion in 2026 and grow to US$ 13.5 billion by 2033, registering a compound annual growth rate (CAGR) of 8.8% during the forecast period. Growing demand for hyperscale facilities, AI-ready infrastructure, and enterprise digital transformation initiatives are fueling market expansion worldwide.

The increasing deployment of high-density computing environments, liquid cooling technologies, and modular data centers is reshaping rack design while creating significant opportunities for manufacturers offering intelligent and AI-optimized rack solutions.

Market Overview

The market has experienced remarkable growth over the last several years. From US$ 4.9 billion in 2020, the industry has steadily expanded due to increasing cloud adoption, remote work trends, IoT deployment, and rapid digital transformation across enterprises.

Modern organizations generate unprecedented amounts of digital information. Applications powered by AI, machine learning, streaming platforms, cloud services, and edge computing require robust infrastructure capable of supporting dense server environments.

As a result, organizations are replacing conventional racks with advanced cabinet systems featuring:

- Integrated cable management

- Intelligent power distribution

- Environmental monitoring

- Enhanced airflow

- Liquid cooling compatibility

- Higher load-bearing capacity

These developments are transforming data center racks from passive infrastructure into intelligent assets supporting next-generation computing environments.

Key Market Highlights

- Market Size (2026): US$ 7.5 Billion

- Projected Market Size (2033): US$ 13.5 Billion

- CAGR (2026–2033): 8.8%

- Leading Region: North America

- Fastest Growing Region: Asia Pacific

- Leading Rack Type: Cabinet Racks

- Fastest Growing Height Segment: Above-42U Racks

- Major Growth Driver: Hyperscale cloud and AI infrastructure expansion

Why the Data Center Rack Market is Growing

Rising Hyperscale Data Center Construction

One of the biggest drivers of the market is the unprecedented construction of hyperscale data centers.

Global cloud providers including:

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- Meta

- Oracle Cloud

continue expanding their infrastructure to support billions of users and enterprise workloads.

These facilities typically require thousands to tens of thousands of rack cabinets, making hyperscale projects among the largest purchasers of rack infrastructure worldwide.

The surge in AI model training and high-performance computing (HPC) further increases demand for specialized racks capable of supporting greater weight, higher power densities, and advanced cooling systems.

AI Infrastructure is Transforming Rack Design

Artificial Intelligence has dramatically changed the requirements of modern data centers.

Traditional server racks typically consumed:

- 5–10 kW per rack

Today's AI infrastructure often requires:

- 30–100+ kW per rack

High-performance NVIDIA GPU clusters require reinforced cabinets capable of supporting increased equipment weight while accommodating liquid cooling systems.

Manufacturers are therefore introducing:

- Direct liquid cooling integration

- Rear-door heat exchangers

- Smart rack monitoring

- High-capacity power distribution

- Improved airflow optimization

AI-ready racks represent one of the highest-value segments within the industry.

Enterprise Digital Transformation

Organizations across industries continue modernizing IT infrastructure to improve operational efficiency and cybersecurity.

Major sectors investing heavily include:

- Banking

- Healthcare

- Manufacturing

- Government

- Retail

- Telecommunications

- Education

Many enterprises are migrating toward hybrid cloud environments, requiring both centralized and edge infrastructure supported by standardized rack systems.

Edge Computing Expansion

Edge computing is another major catalyst.

Instead of processing information solely in centralized cloud facilities, organizations increasingly process data closer to users and connected devices.

Applications include:

- Smart factories

- Retail analytics

- Autonomous vehicles

- Connected healthcare

- Industrial IoT

- Smart cities

Each edge location requires compact rack systems for housing networking equipment, storage devices, and servers.

As 5G deployment accelerates globally, edge infrastructure is expected to become one of the fastest-growing rack deployment opportunities.

Market Challenges

High Cost of Advanced Rack Infrastructure

Modern AI-ready rack systems include sophisticated technologies such as:

- Intelligent monitoring

- Integrated PDUs

- Liquid cooling support

- Heavy-duty structural reinforcement

- Environmental sensors

These premium systems often cost several times more than conventional open-frame racks.

For organizations operating under strict capital expenditure budgets, upgrading entire rack fleets can become financially challenging.

Legacy Data Centers

Many existing enterprise facilities were designed for power densities between 5 and 10 kW per rack.

Today's AI applications frequently exceed 50–100 kW per rack.

Supporting these workloads often requires expensive upgrades to:

- Electrical infrastructure

- Cooling systems

- Raised flooring

- Rack support structures

These modernization costs may delay adoption among organizations operating legacy facilities.

Emerging Opportunities

AI-Optimized Rack Cabinets

The rapid commercialization of generative AI is creating enormous opportunities for manufacturers capable of delivering purpose-built AI rack systems.

Leading vendors are developing rack cabinets featuring:

- Integrated liquid cooling

- Higher weight capacity

- Enhanced airflow

- Intelligent sensors

- AI workload optimization

As AI deployments expand across industries, demand for premium rack solutions is expected to accelerate significantly.

Liquid Cooling Adoption

Traditional air cooling is increasingly insufficient for supporting next-generation AI clusters.

Liquid cooling technologies improve:

- Energy efficiency

- Cooling performance

- Rack density

- Operational reliability

Manufacturers integrating direct liquid cooling into rack designs are expected to capture significant market share during the forecast period.

Telecom and 5G Infrastructure

Global 5G rollout requires thousands of distributed edge data centers supporting ultra-low latency applications.

Telecommunications companies continue deploying compact racks across:

- Cell towers

- Network hubs

- Edge facilities

- Smart manufacturing sites

This trend opens significant opportunities for suppliers of ruggedized and wall-mounted rack systems.

Market Segmentation

By Rack Type

Cabinet Racks

Cabinet racks account for approximately 62% of the market and remain the preferred choice for enterprise and hyperscale facilities.

Advantages include:

- Physical security

- Better airflow management

- Integrated cable organization

- Improved equipment protection

- Compliance with industry standards

Their enclosed architecture makes them ideal for mission-critical environments.

Open Frame Racks

Although lower in cost, open-frame racks are generally used where physical security is less critical, such as testing environments and telecommunications installations.

By Height

42U Racks

The 42U rack remains the industry standard with nearly 58% market share.

Its popularity stems from:

- Universal compatibility

- Ease of maintenance

- Efficient equipment organization

- Standardization across server manufacturers

Above-42U Racks

Larger rack configurations are growing rapidly because AI infrastructure requires higher equipment density and greater load capacity.

These taller systems maximize computing power while reducing floor space requirements.

By Width

19-Inch Racks

Approximately 78% of installations utilize the standard 19-inch width.

This format supports compatibility with nearly all major IT equipment manufacturers.

23-Inch Racks

These remain primarily used within telecommunications infrastructure where legacy equipment requires wider mounting configurations.

By Industry Vertical

The IT and Telecommunications sector represents the largest customer segment.

Cloud providers, telecom operators, internet companies, and managed service providers purchase enormous quantities of standardized rack cabinets every year.

Other significant industries include:

- Healthcare

- Manufacturing

- Government

- Financial Services

- Retail

- Education

Regional Analysis

North America

North America remains the world's largest market.

Growth is supported by:

- Large hyperscale cloud investments

- Government IT modernization

- AI infrastructure deployment

- Federal cybersecurity initiatives

The United States hosts the highest concentration of hyperscale data centers globally, making it the largest individual national market.

Major deployment hubs include:

- Northern Virginia

- Texas

- Arizona

- Nevada

These locations continue attracting substantial investments from leading cloud providers.

Europe

Europe represents a mature market emphasizing sustainability and energy efficiency.

Key growth factors include:

- Green data center initiatives

- Energy efficiency regulations

- Cloud expansion

- Enterprise modernization

Major regional hubs include:

- Frankfurt

- London

- Amsterdam

- Dublin

- Paris

Germany remains Europe's largest rack market due to its extensive data center ecosystem and strong domestic manufacturing base.

Asia Pacific

Asia Pacific is projected to record the fastest growth during the forecast period.

Several factors support regional expansion:

- Rapid cloud adoption

- Government digital initiatives

- AI investments

- Growing internet population

- Expansion of hyperscale facilities

China

China dominates regional demand through major cloud providers including:

- Alibaba Cloud

- Tencent Cloud

- Huawei Cloud

Large government-backed digital infrastructure projects continue driving demand for high-density rack systems.

India

India is becoming one of the world's fastest-growing data center markets.

Programs such as:

- Digital India

- National Data Center initiatives

along with investments from AWS, Microsoft, and Google continue stimulating infrastructure development across major metropolitan regions including Mumbai, Chennai, Hyderabad, and Pune.

Japan

Japan emphasizes premium, earthquake-resistant rack infrastructure capable of supporting highly reliable enterprise and government deployments.

Competitive Landscape

The global data center rack market remains moderately consolidated, with established infrastructure providers maintaining strong market positions.

Key competitive factors include:

- AI-ready designs

- Intelligent monitoring

- Modular architecture

- Compliance certifications

- Liquid cooling compatibility

- Faster deployment capabilities

Manufacturers increasingly compete by offering integrated infrastructure solutions rather than standalone rack products.

Recent Industry Developments

Recent innovations demonstrate the industry's focus on AI and high-density computing.

- Schneider Electric introduced advanced AI-focused rack systems supporting direct-to-chip liquid cooling, increased weight capacity, and larger cabinet dimensions for next-generation compute environments.

- Vertiv strengthened its market position by acquiring Great Lakes Data Racks & Cabinets for approximately US$200 million, expanding its portfolio of integrated rack infrastructure solutions.

These developments reflect growing industry investment in AI-ready data center infrastructure.

Leading Companies

Major participants operating in the global data center rack market include:

- AMCO Enclosures

- Belden Inc.

- Chatsworth Products

- Cisco Systems Inc.

- Dell Inc.

- Eaton Corporation

- Fujitsu

- Hewlett Packard Enterprise

- IBM

- Legrand

- Panduit Corp.

- Rittal GmbH & Co. KG

- Schneider Electric

- Vertiv Group Holdings

These companies continue investing in intelligent rack technologies, modular infrastructure, energy-efficient designs, and AI-optimized cabinet systems to strengthen their competitive positions.

Future Outlook

The future of the data center rack market will be shaped by AI, cloud computing, edge infrastructure, and sustainability initiatives. As enterprises and hyperscale providers deploy increasingly powerful computing systems, conventional rack infrastructure will continue evolving toward intelligent, high-density, and liquid-cooled solutions.

Demand for modular deployments, real-time environmental monitoring, digital twin capabilities, and energy-efficient designs will further transform rack infrastructure into a strategic component of modern data centers.

With hyperscale expansion, rapid AI adoption, and accelerating digital transformation across industries, the global data center rack market is well-positioned for steady long-term growth through 2033. Organizations that invest in scalable, intelligent, and AI-ready rack solutions will be better equipped to support the next generation of digital services while improving operational efficiency, reliability, and sustainability.