Subscriber Data Management Market Overview

The global Subscriber Data Management (SDM) market is entering a period of remarkable expansion as telecommunications providers modernize their networks to support 5G, cloud-native architectures, and billions of connected devices. Subscriber data has become one of the most valuable assets for telecom operators, enabling seamless authentication, personalized services, network optimization, and secure identity management across digital ecosystems.

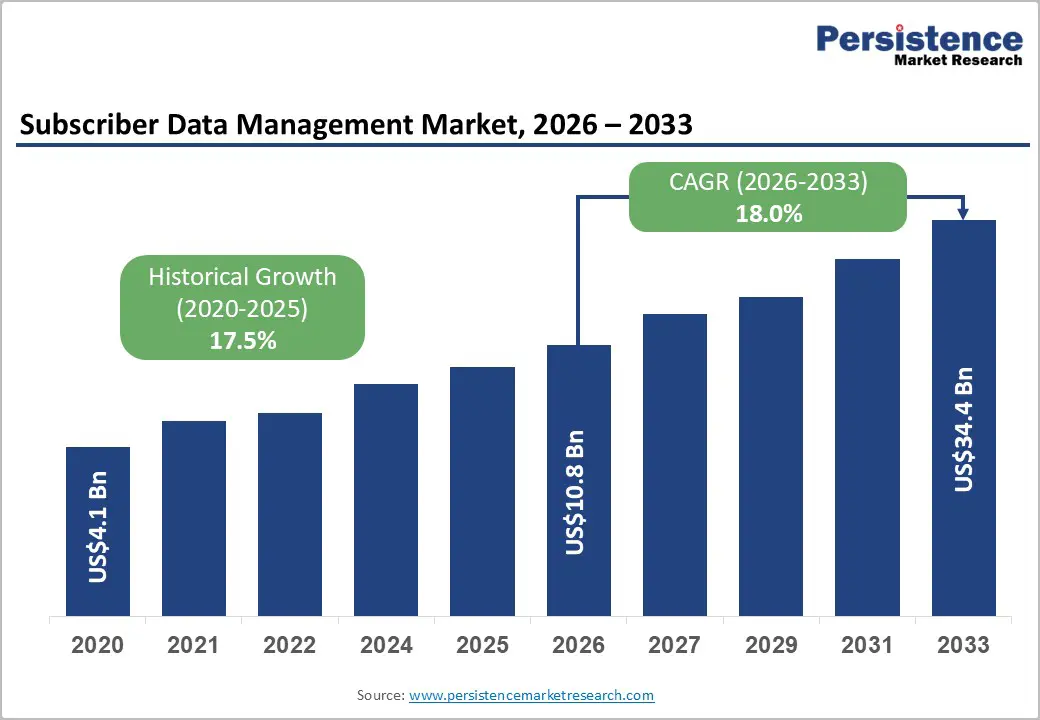

According to recent market analysis, the global subscriber data management market is projected to grow from US$10.8 billion in 2026 to US$34.4 billion by 2033, registering a robust CAGR of 18.0% during the forecast period.

The market's growth is being fueled by several transformative trends, including explosive 5G adoption, the proliferation of more than 18 billion IoT-connected devices globally in 2026, migration toward cloud-native telecom cores, increasing demand for AI-driven subscriber analytics, and evolving regulatory frameworks such as GDPR, the EU Data Act, and national data sovereignty initiatives.

What is Subscriber Data Management?

Subscriber Data Management (SDM) refers to the centralized management of subscriber identities, authentication credentials, service profiles, policies, and network information across telecom infrastructures.

Modern SDM platforms enable telecom operators to:

- Store unified subscriber profiles

- Authenticate users securely

- Enforce Quality of Service (QoS)

- Manage network slicing

- Support roaming services

- Enable personalized customer experiences

- Improve network efficiency

- Facilitate AI-driven analytics

Unlike traditional Home Subscriber Server (HSS) platforms designed primarily for 4G LTE networks, today's cloud-native SDM solutions support both 4G and 5G core architectures, making them indispensable for next-generation telecom networks.

Market Size and Growth Outlook

The Subscriber Data Management market is witnessing sustained investments from telecom operators worldwide.

Market Highlights

- Market Size (2026): US$10.8 Billion

- Projected Market Size (2033): US$34.4 Billion

- CAGR (2026–2033): 18.0%

- Largest Regional Market: North America

- Fastest Growing Region: Asia Pacific

- Leading Solution: Policy Management

- Largest Network Type: Mobile Networks

The increasing need to support billions of mobile users, enterprise IoT deployments, and cloud-native telecom ecosystems will continue driving SDM investments throughout the forecast period.

Key Market Drivers

Rapid Global 5G Deployment

One of the strongest growth drivers is the accelerated rollout of 5G Standalone (SA) networks worldwide.

More than 50 countries have already launched commercial 5G Standalone services, while global 5G subscriptions surpassed 1.6 billion by the end of 2024.

Unlike legacy LTE architectures, 5G introduces:

- Service-Based Architecture (SBA)

- Network slicing

- Dynamic policy management

- Ultra-low latency

- Massive machine communications

These capabilities require real-time subscriber data orchestration, which legacy HSS systems cannot efficiently deliver.

As a result, telecom operators are replacing traditional subscriber databases with cloud-native Unified Data Management (UDM) and Subscriber Data Management platforms.

Growing Number of IoT Devices

The Internet of Things continues to reshape telecommunications.

With more than 18 billion connected IoT devices expected globally in 2026, operators must manage:

- Industrial sensors

- Smart cities

- Connected vehicles

- Healthcare devices

- Smart homes

- Enterprise IoT infrastructure

Each connected device requires secure authentication, identity management, policy enforcement, and real-time connectivity.

Modern SDM solutions provide centralized management of these massive device ecosystems.

Cloud-Native Telecom Transformation

Telecom operators are increasingly migrating toward:

- Cloud-native cores

- Containerized infrastructure

- Kubernetes deployment

- Open APIs

- Microservices architecture

Cloud-native SDM platforms offer:

- Better scalability

- Faster service deployment

- Lower operational costs

- Higher availability

- Improved disaster recovery

This transition is significantly increasing demand for advanced subscriber data management solutions worldwide.

Market Restraints

Data Privacy and Regulatory Compliance

Subscriber information is highly sensitive.

Governments worldwide continue strengthening privacy regulations, including:

- GDPR

- EU Data Act

- National Data Sovereignty Laws

- Regional data localization requirements

Telecom operators must ensure subscriber information remains stored within authorized jurisdictions while maintaining seamless roaming services.

Compliance requires significant investment in:

- Distributed databases

- Encryption

- Identity management

- Secure cloud infrastructure

- Data governance frameworks

These requirements increase deployment costs and implementation complexity.

Vendor Lock-In Concerns

Many SDM platforms remain tightly integrated with proprietary telecom ecosystems.

Migrating subscriber databases between vendors often involves:

- Complex data migration

- Network revalidation

- Operational downtime

- High implementation costs

- Service disruption risks

Consequently, many operators delay modernization initiatives until clear migration strategies become available.

Emerging Opportunities

AI-Powered Subscriber Analytics

Artificial Intelligence is becoming a major competitive differentiator within SDM platforms.

AI enables telecom providers to:

- Predict subscriber churn

- Personalize service offerings

- Improve customer retention

- Optimize network performance

- Detect fraud

- Automate policy management

Machine learning algorithms continuously analyze subscriber behavior to deliver highly personalized services while maximizing operator revenues.

Growth of VoIP and Video over IP

Cloud communications continue expanding rapidly.

Applications such as:

- VoLTE

- VoNR

- Enterprise UCaaS

- Video conferencing

- Streaming services

require secure identity management and real-time Quality of Service.

Modern SDM platforms ensure seamless authentication while maintaining high-quality communications across IP-based networks.

Solution Insights

Policy Management Leads the Market

Policy Management is expected to account for approximately 33% of market revenue in 2026.

Policy engines have become central components of 5G infrastructure because they enable:

- Dynamic QoS enforcement

- Subscriber-specific service control

- Network slicing management

- Service orchestration

- Bandwidth allocation

Companies including Ericsson have integrated advanced policy management capabilities into their cloud-native 5G Core platforms, helping operators deliver differentiated customer experiences.

User Data Repository (UDR) is the Fastest Growing Segment

The User Data Repository represents one of the fastest-growing solution categories.

UDR provides centralized storage for:

- Subscriber profiles

- Authentication credentials

- Service entitlements

- Policy rules

- Device identities

Cloud-native UDR platforms support unified subscriber management across both LTE and 5G environments, making them essential for telecom modernization.

Network Type Analysis

Mobile Networks Dominate

Mobile networks are expected to contribute more than 62% of global market revenue in 2026.

The rapid deployment of 5G Standalone cores has significantly increased demand for:

- Subscriber authentication

- Identity management

- Policy enforcement

- Roaming support

- Network slicing

Leading operators including China Mobile, Verizon, and AT&T continue investing heavily in advanced SDM infrastructure.

Fixed Networks Show Strong Growth

Although mobile remains dominant, fixed broadband infrastructure is expanding rapidly.

The growing adoption of:

- Fiber-to-the-Home (FTTH)

- Fixed-Mobile Convergence (FMC)

- Gigabit broadband

is increasing demand for unified subscriber data platforms capable of managing both fixed and wireless subscribers.

Application Analysis

Mobile Applications Remain the Largest Segment

Mobile applications continue driving SDM demand due to increasing consumption of:

- Video streaming

- Mobile gaming

- E-commerce

- Social media

- Digital banking

- Enterprise mobility

Real-time subscriber management enables telecom operators to provide uninterrupted user experiences even during periods of heavy network congestion.

VoIP and Video over IP are Growing Rapidly

The fastest-growing application area includes:

- Unified communications

- Video conferencing

- Cloud telephony

- Enterprise collaboration

- Voice over LTE

- Voice over New Radio

As organizations adopt hybrid work environments, demand for reliable cloud communications continues increasing globally.

Regional Analysis

North America Leads the Global Market

North America is expected to account for approximately 36% of the Subscriber Data Management market in 2026.

Growth is supported by:

- Early 5G deployment

- Cloud-native network adoption

- High smartphone penetration

- Strong OTT ecosystem

- Large enterprise digital transformation

Major telecom providers continue investing in subscriber analytics and AI-powered network management.

United States

The United States dominates the regional market.

Leading telecom operators including:

- AT&T

- Verizon

- T-Mobile

are modernizing their 5G core infrastructure with cloud-native SDM platforms capable of managing millions of subscribers and connected devices.

Canada

Canada continues expanding its SDM ecosystem through:

- 5G rollout

- IoT adoption

- Government-backed digital infrastructure

- Rural broadband expansion

Europe Maintains Strong Growth

Europe remains the second-largest regional market.

Growth is supported by:

- GDPR compliance

- EU Data Act implementation

- Industrial IoT

- Cloud-native telecom modernization

- Enterprise 5G deployment

Germany

Germany leads Europe's SDM market through strong investments in:

- Industry 4.0

- Private 5G

- Smart manufacturing

- Industrial IoT

United Kingdom

The UK continues adopting advanced subscriber management platforms to support:

- Consumer 5G

- Enterprise mobility

- AI-driven personalization

- Data privacy compliance

Asia Pacific Emerges as the Fastest-Growing Region

Asia Pacific is expected to register the highest growth throughout the forecast period.

Major growth factors include:

- Massive mobile subscriber base

- Expanding 5G infrastructure

- Government digital initiatives

- Rapid IoT adoption

- Cloud-native telecom investments

China

China remains one of the world's largest SDM markets due to:

- Nationwide 5G deployment

- Smart cities

- Industrial IoT

- AI-powered telecom services

India

India represents one of the fastest-growing opportunities.

Key growth drivers include:

- Rapid 5G rollout

- Expanding smartphone users

- Digital India initiatives

- Enterprise private networks

- Growing cloud adoption

Competitive Landscape

The Subscriber Data Management market is moderately consolidated.

Leading companies continue investing in:

- Cloud-native platforms

- AI-powered subscriber analytics

- Open APIs

- Telecom cybersecurity

- Network slicing

- Unified Data Management (UDM)

Major market participants include:

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Oracle Corporation

- Amdocs Limited

- Mavenir Systems, Inc.

- Netcracker Technology

- Comarch S.A.

- Cisco

- Samsung Networks

- Hewlett-Packard Enterprise

- Openwave Mobility

- Casa Systems

Competition increasingly revolves around interoperability, AI capabilities, and cloud-native architecture rather than traditional hardware offerings.

Recent Industry Development

A notable industry milestone occurred in February 2023, when Enea AB joined the Microsoft Azure Operator Nexus Ready Program.

Through this collaboration, Enea integrated its Subscriber Data Management and traffic management solutions—including Subscription Manager and Stratum Data Layer—into Microsoft's Azure ecosystem, enabling operators to accelerate cloud-native 4G and 5G deployments.

Future Outlook

The future of the Subscriber Data Management market will be defined by intelligent automation, AI-driven analytics, cloud-native infrastructure, and expanding 5G ecosystems. As telecom operators continue transitioning from legacy HSS systems to Unified Data Management platforms, SDM will become the foundation for personalized services, secure authentication, network slicing, and real-time policy enforcement.

Growing IoT adoption, enterprise digital transformation, edge computing, and evolving data privacy regulations will further accelerate investments in modern subscriber management platforms. Companies that deliver scalable, interoperable, and AI-enabled SDM solutions will be well positioned to capitalize on the market's strong growth trajectory through 2033.