Introduction: Cybersecurity Market Accelerates Amid Rising Digital Threats

The global cybersecurity market is entering a period of significant expansion as organizations worldwide prioritize digital resilience, data protection, and threat prevention. The increasing frequency of ransomware attacks, sophisticated nation-state cyber operations, rapid cloud adoption, and growing regulatory requirements are transforming cybersecurity from an IT function into a strategic business priority.

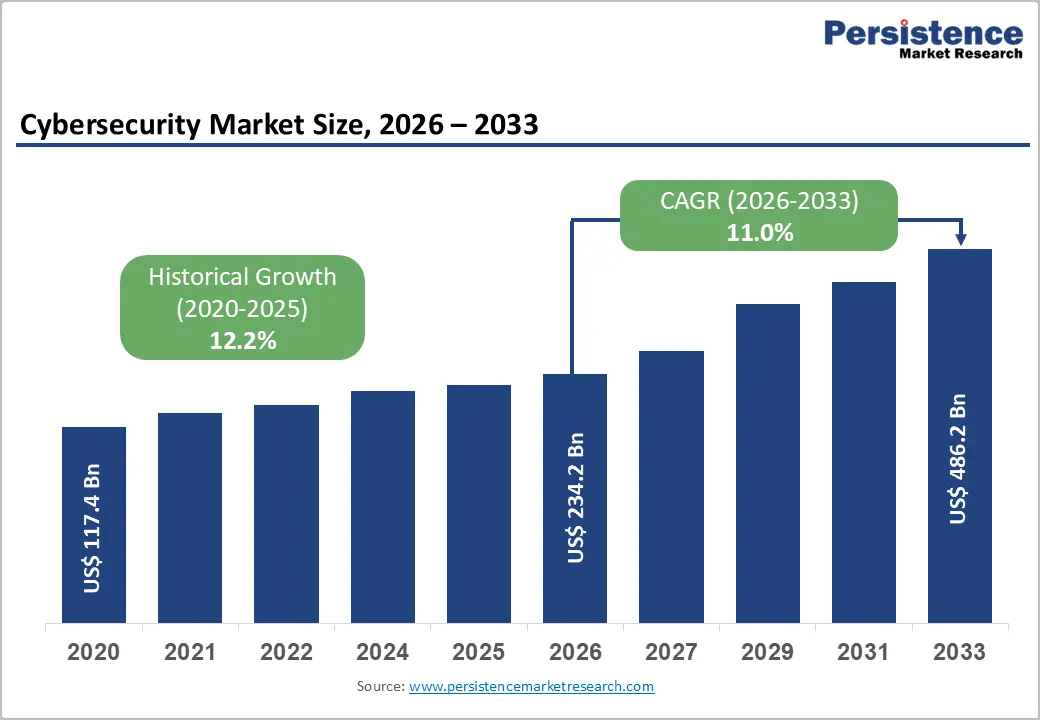

The global cybersecurity market size is expected to reach US$ 234.2 billion in 2026 and is projected to grow to US$ 486.2 billion by 2033, expanding at a CAGR of 11.0% between 2026 and 2033. The market was valued at US$ 117.4 billion in 2020, registering a historical CAGR of 12.2%, supported by accelerated digital transformation, remote work adoption, and increased enterprise vulnerability following the COVID-19 pandemic.

Modern enterprises are facing increasingly complex cyber risks as business operations become more dependent on cloud platforms, connected devices, artificial intelligence, and distributed digital ecosystems. As attack surfaces continue to expand, organizations are investing heavily in advanced security solutions, including extended detection and response (XDR), zero-trust security frameworks, cloud security platforms, identity management solutions, and AI-powered threat detection systems.

Cybersecurity Market Size and Forecast Highlights

The cybersecurity industry is experiencing sustained growth due to the convergence of multiple factors, including:

- Increasing ransomware attacks targeting enterprises and critical infrastructure

- Growing adoption of cloud computing and hybrid work environments

- Rising regulatory compliance requirements across industries

- Increased cybersecurity spending by governments and enterprises

- Integration of artificial intelligence into security operations

North America remains the largest cybersecurity market globally, accounting for approximately 40% market share in 2025, supported by strong enterprise security spending, advanced cybersecurity infrastructure, and the presence of major technology providers.

Asia Pacific is expected to be the fastest-growing regional market, expanding at approximately 13.2% CAGR through 2033, driven by rapid digital transformation, increasing internet penetration, regulatory developments, and rising cyber threats across emerging economies.

Key Market Growth Drivers

Rising Ransomware Attacks and Cybercrime Activities Fuel Security Investments

The rapid increase in ransomware attacks has become one of the strongest drivers of cybersecurity market growth. Cybercriminal groups are increasingly adopting ransomware-as-a-service (RaaS) models, allowing even inexperienced attackers to launch sophisticated campaigns against organizations.

According to the FBI Internet Crime Complaint Center (IC3), cybercrime-related financial losses in the United States exceeded US$ 12.5 billion in 2023, highlighting the growing economic impact of digital threats.

Critical sectors such as healthcare, banking, energy, and government infrastructure have become primary targets due to the high value of their data and operational importance. Successful attacks on hospitals, financial institutions, and public infrastructure have encouraged organizations to increase cybersecurity budgets and implement proactive defense mechanisms.

Enterprises are increasingly adopting solutions such as:

- Endpoint detection and response (EDR)

- Managed detection and response (MDR)

- Security information and event management (SIEM)

- Zero-trust security architecture

- Threat intelligence platforms

As cyberattacks become more frequent and sophisticated, cybersecurity spending is shifting from reactive protection toward continuous monitoring and automated threat prevention.

Regulatory Compliance and Zero-Trust Adoption Accelerate Market Expansion

Government regulations and cybersecurity frameworks are becoming major contributors to market growth. Organizations across industries are required to strengthen security practices to comply with evolving data protection and risk management standards.

In the United States, Executive Order 14028 on Improving the Nation’s Cybersecurity has accelerated zero-trust adoption across federal agencies. The Cybersecurity and Infrastructure Security Agency (CISA) continues to promote stronger cybersecurity practices for government organizations and critical infrastructure providers.

Similarly, Europe’s NIS2 Directive expands cybersecurity obligations across more than 160,000 entities operating in critical sectors. The Digital Operational Resilience Act (DORA) requires financial institutions to improve technology risk management and incident response capabilities.

These regulations are driving demand for:

- Identity and access management (IAM)

- Data loss prevention (DLP)

- Security monitoring platforms

- Encryption solutions

- Compliance management tools

Regulatory pressure has transformed cybersecurity solutions from optional investments into mandatory business requirements.

Market Restraints

Global Cybersecurity Talent Shortage Limits Security Deployment

Despite increasing cybersecurity investments, the shortage of skilled cybersecurity professionals remains a major challenge for organizations.

According to ISC2, the global cybersecurity workforce gap reached approximately 4 million professionals in 2023. Many organizations struggle to recruit experienced security analysts, engineers, and incident response specialists capable of managing complex security environments.

This shortage creates several challenges:

- Delayed implementation of security solutions

- Inefficient monitoring of security alerts

- Increased dependence on managed security service providers

- Higher operational costs

Although cybersecurity technologies are becoming more advanced, organizations require skilled professionals to configure, manage, and optimize these platforms effectively.

The talent shortage is encouraging enterprises to adopt AI-powered security automation and outsourced cybersecurity services to reduce operational pressure.

Complexity of Multi-Vendor Security Environments

Large organizations often operate dozens of cybersecurity tools from multiple vendors, creating integration challenges and operational inefficiencies.

Enterprises commonly deploy separate solutions for:

- Network security

- Endpoint protection

- Cloud security

- Identity management

- Threat intelligence

- Data protection

However, fragmented security environments can create visibility gaps and increase alert fatigue among security teams.

This challenge is driving demand for integrated cybersecurity platforms that combine multiple capabilities into unified ecosystems. Companies such as Microsoft, Palo Alto Networks, CrowdStrike, and Cisco are increasingly focusing on platform-based strategies to simplify enterprise security management.

Emerging Opportunities in the Cybersecurity Market

Artificial Intelligence Transforming Cybersecurity Operations

Artificial intelligence is becoming one of the most transformative technologies in the cybersecurity industry. AI-powered platforms can analyze massive volumes of security data, identify abnormal behavior, and automate threat response processes.

Generative AI solutions such as:

- Microsoft Security Copilot

- CrowdStrike Charlotte AI

- Palo Alto Networks Cortex XSIAM

are helping security teams improve productivity and reduce response times.

AI-driven cybersecurity enables:

- Automated threat detection

- Faster incident investigation

- Predictive security analytics

- Intelligent vulnerability management

With the cybersecurity workforce shortage expected to continue, AI-based security automation represents a major growth opportunity for technology providers.

Cloud Security and SASE Adoption Create New Growth Opportunities

The rapid transition toward cloud computing and hybrid work models has expanded enterprise attack surfaces. Organizations are increasingly adopting cloud-native security solutions to protect distributed applications, workloads, and users.

Cloud security solutions such as:

- Cloud Security Posture Management (CSPM)

- Cloud Workload Protection Platforms (CWPP)

- Secure Access Service Edge (SASE)

- Cloud Access Security Broker (CASB)

are gaining strong adoption.

The Secure Access Service Edge (SASE) framework combines networking and security capabilities through cloud-based architectures, enabling organizations to secure remote employees and distributed applications.

Leading providers, including Microsoft, Palo Alto Networks, Zscaler, and Fortinet, are expanding their cloud security portfolios to capture this growing demand.

Cybersecurity Market Segment Analysis

Software Segment Leads the Market

Software represents the dominant component category, accounting for approximately 45% market share in 2025.

Cybersecurity software continues to gain traction due to the increasing adoption of subscription-based security platforms and cloud-native delivery models.

Major software categories include:

- Identity and access management

- SIEM platforms

- Endpoint security

- XDR solutions

- Encryption software

Leading cybersecurity companies are increasingly moving toward integrated platforms that provide multiple security capabilities through a single ecosystem.

Network Security Remains a Leading Security Type

Network security accounts for approximately 22% market share in 2025, making it one of the largest cybersecurity segments.

Network security solutions remain essential because cyber threats often enter organizations through network infrastructure.

Key solutions include:

- Next-generation firewalls

- Intrusion prevention systems

- Network monitoring tools

- VPN security solutions

Companies such as Cisco, Fortinet, Palo Alto Networks, and Check Point continue to dominate this segment.

Cloud-Based Deployment Gains Market Leadership

Cloud-based cybersecurity deployment accounted for approximately 52% market share in 2025.

Organizations are increasingly choosing cloud security platforms because they provide:

- Faster deployment

- Lower infrastructure costs

- Continuous updates

- Scalability across global operations

Cloud-based cybersecurity adoption is particularly strong among enterprises transitioning toward hybrid and multi-cloud environments.

Regional Market Insights

North America Cybersecurity Market

North America dominates the global cybersecurity market with around 40% market share in 2025.

The region benefits from:

- High cybersecurity spending among enterprises

- Strong government security initiatives

- Presence of leading cybersecurity companies

- Advanced digital infrastructure

The United States represents approximately 82% of North American cybersecurity revenue.

Growing cyber threats, SEC cybersecurity disclosure requirements, and federal cybersecurity initiatives are supporting continued market expansion.

Europe Cybersecurity Market

Europe is experiencing strong cybersecurity growth due to regulatory developments including:

- NIS2 Directive

- GDPR enforcement

- Digital Operational Resilience Act

- Cyber Resilience Act

Germany, the United Kingdom, and France represent major cybersecurity markets in the region.

Organizations across financial services, manufacturing, and government sectors are increasing security investments to meet compliance requirements.

Asia Pacific Cybersecurity Market

Asia Pacific is the fastest-growing cybersecurity region, projected to expand at approximately 13.2% CAGR through 2033.

Growth is supported by:

- Digital transformation initiatives

- Increasing cybercrime activity

- Government cybersecurity programs

- Expansion of cloud infrastructure

India is emerging as a major cybersecurity market, supported by the Digital Personal Data Protection Act 2023 and increasing enterprise digitization.

Japan, China, Singapore, and Southeast Asian countries are also increasing cybersecurity investments to protect growing digital economies.

Competitive Landscape

The cybersecurity market is moderately consolidated, with major technology companies competing through integrated security platforms, artificial intelligence capabilities, and cloud-based solutions.

Key market players include:

- Microsoft Corporation

- Palo Alto Networks

- CrowdStrike

- Cisco Systems

- Fortinet

- IBM Corporation

- Check Point Software Technologies

- Trend Micro

- Zscaler

- SentinelOne

- Cloudflare

- Broadcom

- Sophos

- Trellix

- Juniper Networks

Companies are increasingly focusing on:

- AI-powered threat detection

- Platform consolidation

- Managed security services

- Cloud security innovation

- Strategic partnerships and acquisitions

Future Outlook of the Cybersecurity Market

The cybersecurity market is expected to maintain strong growth through 2033 as digital transformation continues across industries. Increasing cyber threats, regulatory requirements, and AI-driven security innovation will remain the primary forces shaping the industry.

Future cybersecurity strategies will increasingly focus on:

- Autonomous threat detection

- Zero-trust security frameworks

- AI-powered security operations

- Cloud-native protection

- Identity-first security models

As organizations continue expanding their digital ecosystems, cybersecurity will become a fundamental requirement for business continuity, operational resilience, and national security.

With the market projected to reach US$ 486.2 billion by 2033, cybersecurity will remain one of the most critical and fastest-evolving technology sectors worldwide.